The UK says a PDF is not an invoice. France just made it one.

ArticleJuly 9, 2026

ArticleJuly 9, 2026

About Benson Hendall, PDFSmart

The views expressed in this article are those of the author(s) and do not reflect the policies or positions of the PDF Association.

In June 2026, HMRC confirmed that the UK’s 2029 e-invoicing mandate will run on the Peppol network, and made clear that a PDF, however well-formed, will not count as an electronic invoice. Weeks from now, France’s own mandate goes live with a hybrid PDF/A-3 format as a first-class citizen of its legal framework. Same term, two philosophies, and a genuine question about what an invoice is for.

One invoice, two legal realities

Picture two finance managers in the autumn of 2027, one in Manchester and one in Lyon, doing exactly the same thing: exporting an invoice as a tidy, letterheaded PDF and emailing it to a domestic business customer. In Manchester, this is still a perfectly ordinary invoice, and will remain one until April 2029. In Lyon, it stopped being one a year earlier: since 1 September 2026, invoices between French businesses must travel as electronic invoices through state-registered platforms, and a plain PDF attached to an email no longer qualifies.

Nothing about the file differs. What differs is the definition. Two neighbouring jurisdictions, wrestling with the same VAT-gap arithmetic and the same automation argument, have arrived at incompatible answers to a deceptively simple question: is a document that a human can read, but a machine cannot reliably parse, an invoice? The UK has answered no. France has answered that it can be both, provided the format does both jobs at once.

What the UK actually decided

The UK’s direction was set at Autumn Budget 2025: from April 2029, all VAT invoices for business-to-business and business-to-government transactions must be issued and received electronically. The consultation response published alongside the Budget is unambiguous about scope: PDFs, Word files, HTML invoices and OCR-scanned images sit expressly outside the definition of e-invoicing. The mandate targets structured, machine-readable invoice data flowing directly between financial systems.

On 23 June 2026, HMRC added the missing technical piece. In its “Tax update 2026: simplification, modernisation and fairness” policy paper, the government confirmed Peppol as the core interoperability network for UK e-invoicing: a decentralised, four-corner model in which suppliers and buyers exchange structured documents through accredited access points, with no central clearance platform and, initially at least, no real-time reporting to HMRC. The full technical standards are still being co-designed with industry, and a detailed implementation roadmap is due at Budget 2026 in November. But the philosophical commitment is already legible: in the UK’s future regime, the invoice is the data. Any human-readable view of it is a presentation-layer courtesy, generated by software on demand.

What France decided instead

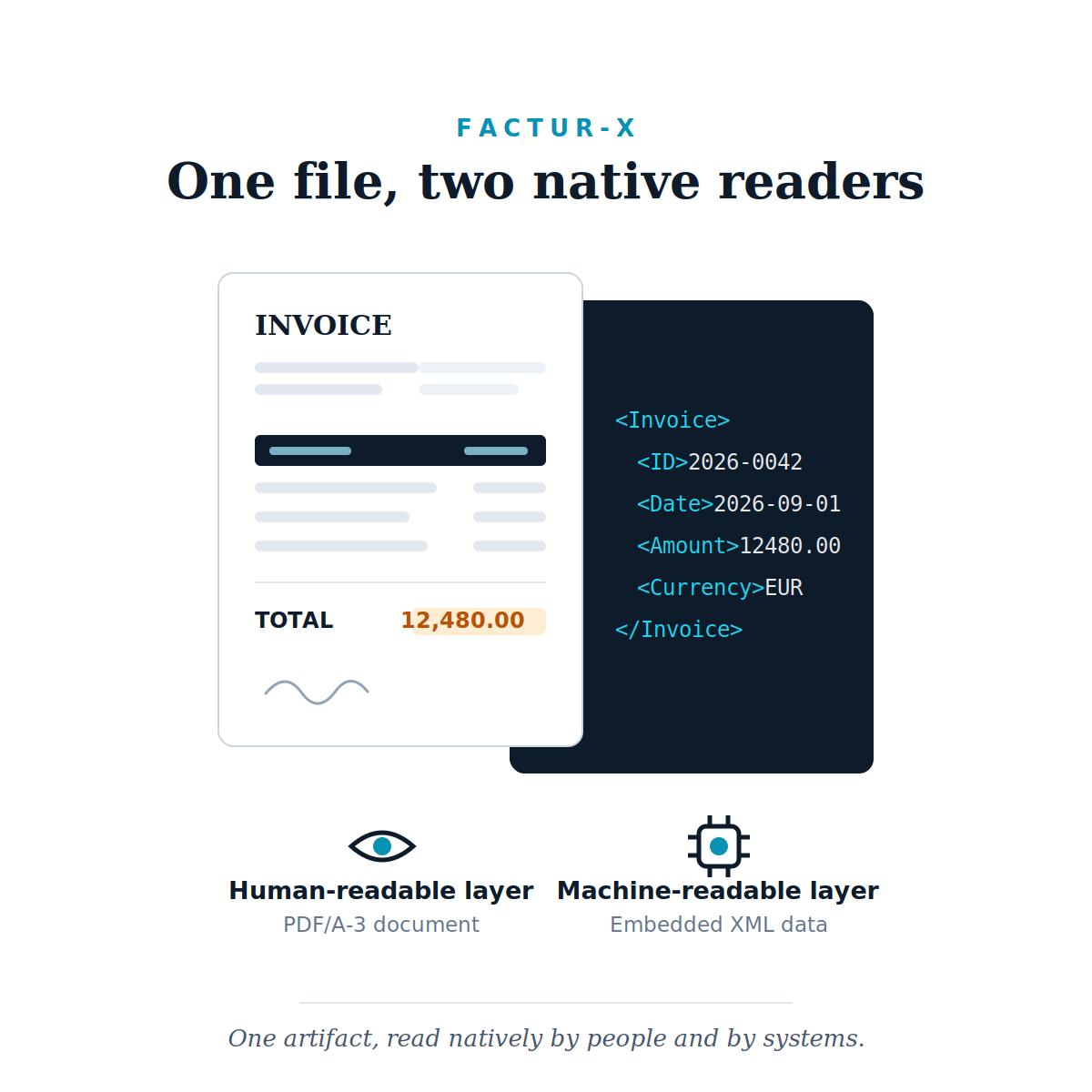

France gets there three years earlier, and by a different route. From 1 September 2026, every business subject to French VAT must be able to receive electronic invoices; large and mid-sized companies must issue them from that date, with smaller businesses following on 1 September 2027. Exchange runs through state-registered platforms (plateformes agréées), and the reform admits three core formats. Two of them, UBL and CII, are purely structured XML. The third is Factur-X.

Factur-X is the interesting one. It is a hybrid: a fully conformant PDF/A-3 document, readable by any human with any PDF viewer, carrying an embedded XML file that machines process directly. The trick is only possible because PDF/A-3 did something its stricter predecessors forbade: it allowed arbitrary files to be embedded within an archival PDF, on the explicit understanding that the PDF remains the authoritative, human-readable rendition of the whole. A Factur-X invoice is therefore one artifact with two native readers. The accountant sees a familiar invoice; the accounts-payable system never touches the pixels and reads the XML. Neither view is a derivative of the other: both are the invoice.

France did not mandate the hybrid; pure UBL or CII are equally valid within its core set. But by placing Factur-X in that set, France made human readability a first-class property of a legal invoice. The UK’s definition excludes it by construction.

Two philosophies of the same document

Strip away the acronyms and the disagreement is philosophical. The UK’s position: an invoice is a record of structured facts, and rendering those facts for human eyes is the software's job: accurate, current, but existing only when summoned. The French hybrid position: an invoice is also evidence, and evidence should be inspectable by an unassisted human being, today and in twenty years, without depending on the software that produced it.

Readers of this site may recognise the shape of this argument. It is the same gap that separates a PDF that renders beautifully from a PDF that machines can actually read: visual fidelity and machine readability are different properties, and assuming one implies the other is where documents quietly fail. E-invoicing regulation is that same gap, promoted from an engineering nuisance to a matter of law. The UK resolves it by abolishing the visual artifact from the definition. Factur-X resolves it by binding the two properties into a single file and refusing to choose.

Both positions are coherent. Pure structured data is lighter, less ambiguous, and cannot drift out of sync with a visual layer; there is no visual layer to drift from. The hybrid costs more bytes and more standardisation effort, but it degrades gracefully: whatever happens to platforms, protocols and vendors, the document still opens.

The archive question nobody is asking

That graceful degradation matters most at the point almost no one in this debate is discussing: year six. UK record-keeping rules require invoices to be retained for six years in a form that guarantees access, readability and retrieval. But the readability of a pure UBL or CII invoice is entirely mediated: it means a stylesheet, a renderer, a platform, or an archived viewer that still runs. None of these are properties of the file. They are properties of an ecosystem around the file, and ecosystems have shorter lifespans than tax retention schedules.

A Factur-X invoice, by contrast, is self-archiving by construction. PDF/A-3 exists precisely to guarantee that a document remains self-contained and renderable decades on; that is the format’s founding contract, and the structured payload rides inside the preservation wrapper. It is a curious irony of the UK’s machine-first definition that it makes the invoice easier to exchange in 2029 and potentially harder for anyone to read in 2039. The roadmap due at Budget 2026 would do well to say as much about retention as it does about transmission.

If you invoice across the Channel

For businesses caught between the two regimes, three practical bearings follow. First, know what your jurisdiction calls an invoice: the same file can be compliant on one side of the Channel and legally invisible on the other, and that divergence is live from this September, not hypothetical. Second, let your counterparties set your real deadline: buyers in mandated markets increasingly ask suppliers for structured invoices as a condition of doing business, whatever domestic law requires and whatever April 2029 permits. Third, do not discard the PDF; requalify it. In one regime it remains the invoice’s legal body; in the other it becomes the human-facing view of a data record. A demotion in law, but not in usefulness.

The mistake, in other words, is not choosing the wrong format. It is assuming that the phrase “PDF invoice” still means anything at all without saying which side of the Channel you are standing on.